We are exactly where we expected to be. The only unanticipated change to the Colorado real estate market is the speed at which we experienced the impact. Seemingly overnight. Yet, we’ve been expecting this since January. There is a direct correlation between the rapid rise in mortgage interest rates in the spring of this year and the decline of buyer activity. This buyer activity decline, along with some sellers motivated to capitalize on rapid appreciation, has led to the sharpest increase in inventory and shift in buying patterns since the 2008 housing crisis.

But let’s be clear, this is a long awaited and welcomed correction, not a crisis.

In this market update, we will look at:

1. Interest rates

2. Buyer activity

3. Market activity

4. Inventory and days on market

5. Home pricing and offer trends

We would be remiss in not acknowledging other economic forces at play. As much as they are exhausting and maybe a little scary to think about, they are important considerations that will have long term affect, ultimately on local conditions. Global food shortages hitting this fall, carbon emissions policies impacting the future of farming, housing and population migration worldwide, United States inflation rates and federal reserve monetary policy to minimize the long-term inflationary impacts balanced with the impact these monetary policies have on spending, borrowing and the equities markets, continued supply chain issues, United States energy dependence and prices, recession and what is likely to be a challenged jobs market in the coming months. And not to mention the political and social climates including mid-term elections. We will not address the technical aspects of these factors affecting Colorado housing but know that any conclusions are taking these factors into account, as unpredictable as many of them are.

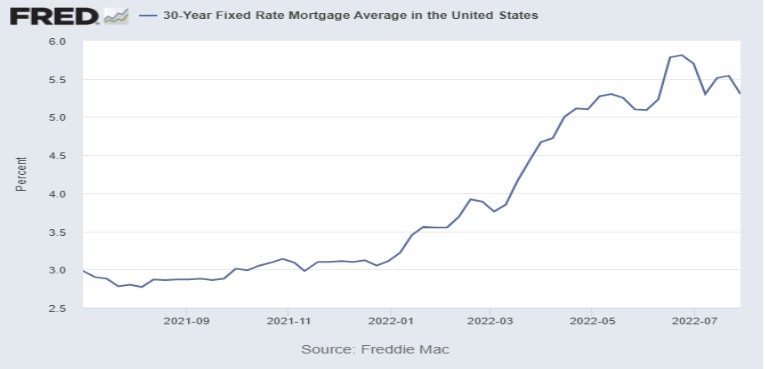

Interest Rates

In the last 12 months, interest rates have moved up as much as 3.5%, from 2.75% on a 30 -year fixed loan to as high as 6.25% early summer. Rates have come back down some, hovering in the high 4’s to mid 5’s.

The practical and emotional reaction of home buyers to this interest rate change has been sudden and profound. The monthly principle and interest cost of a $500,000 loan went from $1,975 to as high as $3,078.

Some buyers could no longer afford to purchase a home in the way they had planned, because the cost of ownership increased so rapidly. For others, they could still afford to buy, but the emotional response to the change in conditions was to pause and, in some cases, quit their home search.

There are solid fundamentals that predict a possible decline of interest rates in the next 18 months, but buyers should behave as if rates will continue to rise.

If rates decline, there will be another wave of buying activity resulting in home values rising sharply. Homeowners who have higher interest rates can refinance at that time. If rates increase from here forward, people who buy today will be happy to have locked in a lower interest rate if they intend to own long term.

One significant adjustment buyers may choose to make is using different loan products to purchase. FHA and ARM (Adjustable Rate Mortgage) loans were virtually non-existent over the last few years. A good mortgage banker will help buyers consider these (and other) product options to understand the potential advantages, which in some cases will reduce capital outlay and cost of ownership.

Buyer Activity

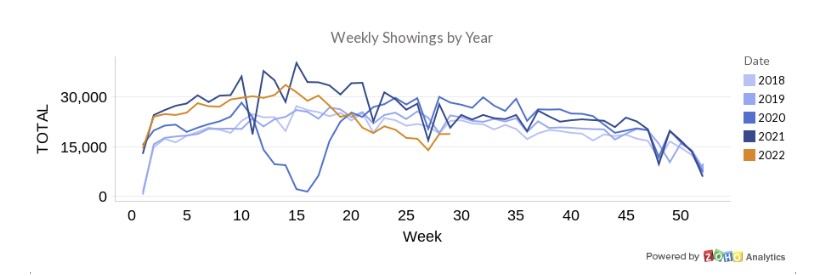

Buyer activity is as low for this time over year as we have records for. Showings have been below 20,000 per week for the last 5 weeks. Much of this is the emotional response to the changing market conditions and will likely normalize over the next couple months.

Until buyer activity recovers, we will continue to see a rise in inventory, price corrections of listings, markedly fewer showings and a growing trend of offers below asking price. Most significantly is the precipitous fall of showings per listing by week. Early 2022 the average listing was experiencing 18 showings per week. As of this week, 2.6 showings per listing.

The above chart demonstrates the need for establishing remarkable expectations and thorough, regular communication between agent and seller. Use this data to help sellers understand market conditions. Your job is not to control or be responsible for market conditions, but a professional will help theconsumer read and adapt to those conditions.

The good news is, we require about the same number of showings to get a home under contract, as we always have. Approximately 18-20 showings (obviously impacted by price range). Look at the average number of showings in the listings price range and geography, and simply do the math. If you are getting 3 showings a week and it takes 18 showings on average to get under contract, marketing time should be about 6 weeks.

If you pass 18 showings and the property is not under contract, it is likely over priced for the condition, features and location.

Market Activity

With the sharp decline in buyer activity, there is a commensurate impact on the market overall. The number of properties going under contract, and number of homes selling each week are at historically low numbers for this time of year and a 40-50% decline compared to the last few years.

Don’t let this scare you. This is when professionals rise. These market conditions will be relatively short lived. And these market conditions cause the lazy and incompetence to get out of the business.

Stay the course and you will have more opportunities in the next 5 years than you have in the last 5 years. You will also experience more appreciation in partnership with your clients because they will again understand the value of a true professional.

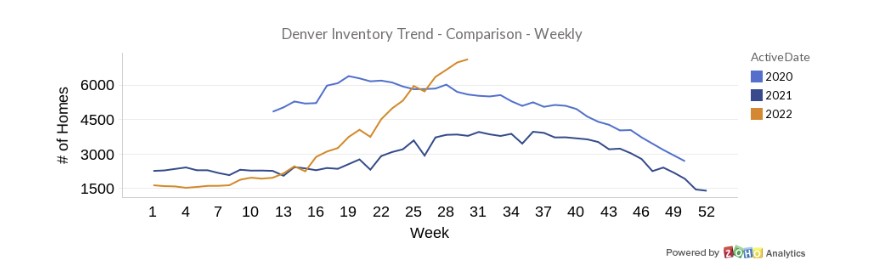

Inventory and Days on Market

Inventory is at its highest level in July (Other than 2019) since 2012. At 7,099 homes available for sale, that is a 5 time increase inventory over January of this year.

Just a quick reminder…we’ve been wanting this for years…

More inventory means not operating at a breakneck pace. It will take you and your clients a little while to adapt, but soon you’ll approach showings very differently than you have the last 5-8 years. You’ll have 20 properties to look at on a Tuesday, and 18 of them will still be there on Saturday.

Days on Market

NO surprise, with decreased buyer activity and increased listing; days on market is increasing. As of July 29, 2022 average days on market is now at 21 days. That’s almost a 4 time increase from just 4 months ago.

Home Pricing and Offer Trends

Home sale prices have been dropping since end of April this year. The high average sale price hit $832,000 for a detached single-family home in March and mostly maintained that level until the beginning of June. Since then, we have seen a decline of the average sales price to $753,000. This is a trend that has occurred every year, other than 2020.

Don’t let sensational headlines fool you. This is NOT (yet) a loss of equity in homes, rather a reduction in the average sales price most likely caused by smaller homes being sold given the time of year. Just a guess, time will tell. We do not see a precipitous fall in home values coming, given current market conditions. There is still a housing shortage, Colorado’s economy remains extremely strong and the anticipated population increase in Colorado will continue to put upward pressure on home prices. Macroeconomic and geo-political factors such as US national debt, inflation, world-wide recession and international conflict

concerns world-wide may ultimately impact Colorado. But remember that Colorado is as insulated as anywhere in the country.

Offer Prices and Price Reductions

The anticipated trend of lower offer prices and prices reductions has kicked into full swing. In March of this year, over 80% of all properties were selling above the asking price with only 11% selling below. As of July 29, only 30% of homes are selling for above the asking price and almost 52% are selling below. Significantly, it’s valuable to note that this data is reflective of market conditions when the properties went under contract, 30-40 days before. It’s reasonable to anticipate trend to continue as

buyers and sellers adjust to these new conditions.

And, we are seeing an acceleration in price reductions. That will most likely continue. In March of this year, only 5% of homes listed for sale ever experienced a price reduction. As of July 29, 32% of all listings are experiencing a price reduction.

Again, use this information to help sellers understand how you will partner with them to read the market, prepare their property, help them price their home and make adjustments based on volume of showings, feedback and their capacity for patience. We are back to real consulting days.

Conclusions:

Every correction has some pain. Some of this pain is practical and financial as some buyers can no longer afford to buy and some sellers won’t be able to sell for what they “need”. For most people however, it is the emotional pain of dealing with market conditions that are simply different and different is often unwelcome.

This emotional adjustment period will most likely take us through September or October of 2022 with residual affects through year end; then consumers and industry professionals will have adapted. Sellers will learn to accept more property preparation, reasonable pricing, and longer marketing times being key to their success.

Buyers will adapt to a higher cost of ownership due to increased interest rates, but also enjoy scheduling showings at a more modest pace compared to the last 5 years and writing offers on homes below the asking price, with little competition. Given market volatility, buyers who are looking to make a quick buck through home value appreciation should not be purchasing in this market. The quick buck days are likely over for the foreseeable future.

Only long-term investors and homeowners in a primary residence should be active in this market. That is most people. Buyers should consider all lending strategies with a highly qualified mortgage banker.

Anticipate that we are not going back, maybe ever, to what we’ve experienced over the last 7 years, certainly not over the last 2 years. Economic and market forces have simply changed, and this industry will operate more similarly to the 2004-2007 market with plenty of properties to choose from, and sellers experiencing modest appreciation of home values with longer marketing times.

Accept these changes and you’ll be just fine.